By Kari Williamson

Global wind energy installed capacity increased at a compound annual growth rate (CAGR) of 27.9% from 74.1 GW in 2006 to 198.2 GW in 2010, of which 36.1 GW came online in 2010. There was a fall in annual additions in 2010 by 10.9%, however, as major wind markets such as the US, Germany and Spain were hit by the global economic crisis.

The global wind power markets are expected to recover in 2011 with the huge order intake by major wind manufacturers, the growing Asia-Pacific region, emerging South America and Africa regions, steady European wind markets and recovery in North America, GlobalData says.

The growing Asia-Pacific wind power market powered by India, China and other emerging countries such as Republic of Korea, Thailand and Philippines will continue to drive the wind power market as well as emerging South America and Africa countries such as Brazil, Columbia, Argentina and South Africa.

China largest in 2010

China was the global leader with a cumulative installed wind power capacity share of 22.6% in 2010, overtaking the US as the number one wind power market in terms of new installations in 2009 following the addition of 13.8 GW of wind capacity in that year.

China has doubled its cumulative capacity every year during 2006-2009 and grew by 72.4% in 2010 after the addition of 18.8 GW of new capacity. Supportive government policies which include an attractive concessional programme and the availability of low cost financing from government banks are critical reasons for the success of the Chinese wind power market, the analyst says.

It is expected that China will continue to promote wind power in order to reduce its carbon footprint and increase rural electrification.

US comes in second

The US is the second largest wind power market with a cumulative share of 20.3% of the global wind power market. Its share decreased by 1.4% in 2010 which lost the US its market supremacy.

Germany is the third largest wind power market in the world with a share of 13.7%. Germany maintained its ranking in 2010 but lost 2.2% to competing nations. Spain, which is the fourth largest wind power market with a cumulative share of 10.4%, lost 1.4% in 2010 as it continued to face economic problems. The other major wind power markets include India with a share of 6.6%, Italy and France with a share of 2.9% each, the UK with 2.6%, Portugal with 2.1% and Canada with 2%.

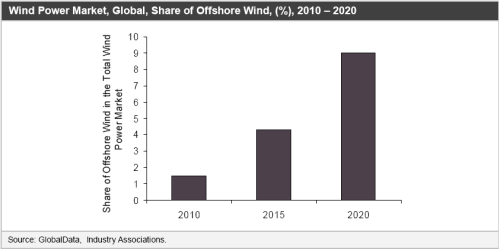

Offshore wind gains momentum from 2015

The offshore wind market is expected to become one of the major market segments of wind power generation during the forecast period. Offshore wind power installations accounted for 1.6% of the global wind power market in 2010.

The UK, Germany, the Netherlands, the US and China are the biggest offshore wind power markets in the world with a number of projects currently in planning and under construction. With an increasing number of countries exploiting offshore wind potential during the forecast period 2010-2020 it is expected that its share in the global wind power market will reach 9% by 2020.

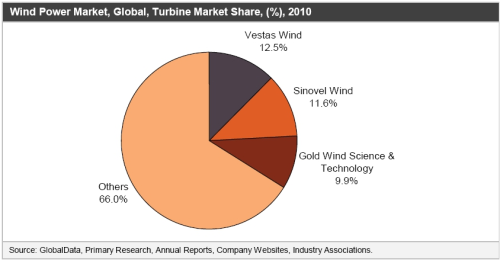

Vestas largest manufacturer in 2010

The global wind turbine market is a consolidated market with the top 10 players accounting for 80.4% of the market. Vestas Wind Systems A/S dominated the global market in 2010 with a 12.5% share and a total of 4719 MW of new turbines installed. The company however lost a share of 0.9% in 2010. Vestas is the industry leader and one of the strongest vertically integrated wind turbine manufacturers.

Chinese giant Sinovel Wind Group Co Ltd was the second largest wind turbine manufacturer in 2010 with a share of 11.6%. The company installed 4386 MW of wind turbines and gained a 2.3% market share. Sinovel is followed by another Chinese turbine manufacturer, Xinjiang GoldWind Science & Technology Co Ltd, which accounted for 9.9% of the market in 2010. The company installed over 3.7 GW of turbines in 2010 and gained a share of 2.7%.

GE Energy, which was the second largest turbine manufacturer in 2009, slipped down to fourth position after losing 2.8% of its market share in 2010. The company accounted for 9.4% of the market in 2010 compared to 12.2% in 2009.

Gamesa Corporacion Tecnologica S.A. accounted for 7.5%, Dongfang Electric Corporation Limited accounted for 6.9%, Enercon GmbH accounted for 6.8%, Guodian United Power Technology accounted for 6.5%, Suzlon Energy accounted for 4.8% and Siemens accounted for 4.6% of the global annual capacity in 2010.

Consolidations on the horizon

The major business strategies adopted by the global manufacturers for long term sustainability in the market are investments in research and development (R&D) to expand existing product portfolios to meet changing market needs, capacity expansions and setting up manufacturing units across regions to cater to local demand.

Consolidation is on the cards as the US market is undergoing correction and the Chinese wind market is expected to stabilise during the forecast period. Companies have modest expectations of growth for 2011 as major markets have slowed down but are expected to pick up in the second half of year.