There is certainly much to celebrate when it comes to Latin America's wind industry. The potential for wind power is especially strong in terms of the raw resources and provides a road for governments to develop a domestic source of energy to complement the region's current dependence on large hydro generation. The region is also adding new projects and capacity at an increasing rate.

Optimists would even say, as Ernst and Young did in its 10th Annual Renewable Energy Attractiveness Index, that “South America is leaving Europe behind”.

Ambitious and optimistic, maybe even over the top, the statement suggests that there is something brewing in South America that can potentially steal the show in the wind industry. Further into the index is another interesting gem: Brazil, says the firm, is losing its status in wind as the country's regulators look to boost other sectors.

Chile, it seems, is the new rising star. This is not based on current capacity, but on its pipeline of projects and potential, E&Y notes. The country rose to the 25th rank in wind, out of 40 countries around the world covered in E&Y's index. Also placing in the financial consultant's index for the first time, Peru reached 26, just ahead of Mexico at 29. Brazil, even if its momentum has slowed, still holds the top ranking in Latin America however, coming in at 15 place overall.

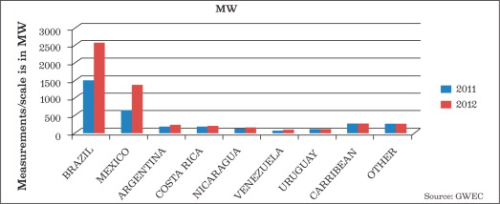

A look at installed capacity doesn't seem to capture the potential in resources. Rather it shows regional growth, but mostly on the back of Brazil. It does however, show record growth in terms of capacity as a region. According to the Global Wind Energy Council (GWEC), in 2012 Latin America added over 1GW for the first time, with six markets installing a combined 1225MW of new wind capacity to give a cumulative regional total of 3.5GW.

Brazil accounted for the majority of growth, adding 1077MW in 2012. The country also has almost 7GW of projects in the pipeline through 2016. Globally, GWEC describes Brazil as “one of the most promising onshore markets for wind energy, at least for the next five years”.

Fundamentals strong, location key

Macros aside, what else is brewing in Latin America's wind market? According to MAKE Consulting's April 2013 Wind Power Market Outlook, Latin America represents “the real opportunity over the next eight years” as the region is set to grow at a compounded annual growth rate of 20%

Driving this demand are the emerging economies of the region, which will have to fill greater energy needs looking forward. This thirst for capacity creates a space for new players as well, and many countries are looking to bolster their domestic energy supply.

MAKE's Latin America analyst Brian Gaylord says that advances in technology experienced in wind equipment coupled with potential sites with great quality wind make the region particularly attractive. Compare this to mature markets, where legacy equipment has taken the best spots.

Governments are looking to increase domestic resources, cutting themselves of their dependence on large-scale hydro projects – which by their very nature are especially susceptible to drought and decreases in rainfall, a regular occurrence thanks to the effects of climate change and El Niño weather pattern.

Wind has been a friendly companion to Latin America's hydro. According to Pacific Hydro CEO Rob Grant, in both markets where the company operators it has benefited from lulls in hydro production, which push the energy price up and tend to lead to greater use of wind power.

Wind power has represented one of the few mass-scale, on-the-grid varieties of renewables. Grant says that while there is potential throughout Latin America, the prime opportunity for creating a wind production scenario that can compete in the broader utilities market is in Brazil. The company is participating in a number of projects and expects over the long term a good part, even a third, of its business to be founded in Brazil as the company moves forward.

Chile, has a need for domestic energy solutions and wind is in the government's long term plan, but Grant emphasizes that to take advantage of this interest, precise positioning to guarantee good wind resources and a connection to the country's main electrical transmission line, the SIC, is critical. In the case of Pacific Hydro, obtaining sufficient long-term data to verify resources and site suitability has been a challenge.

Pacific Hydro spent a good three years evaluating potential wind farm sites before making a move. Its main project in Chile is a 106MW farm, Punta Sierra, located in Chile's north, near the city of Coquimbo. Failing to do good due diligence, the CEO says, could result in disappointing results once the projects are online.

Financing as a vendor

MAKE's Gaylord says the primary lenders are development banks, both local and international. The Chinese, looking to deploy turbines from its industry, are using cheap loans to compete with other manufacturers like Vestas or GE.

To do this, Chinese lenders are using low rates to rake in some of the region's biggest developments. The Chinese Development Bank (CDB) is reported to be the financer of a US$3.5bn wind farm project in Argentina that unites Generadora Eólica Argentina del Sur S.A. (GEASSA) and Beijing Construction Engineering Group International (BCEGI).

GEASSA didn't specify the source of its loan, but Bloomberg reported that CDB is offering financing at up to 50% less than local options. Add politics, as GEASSA said at the time that the then premier of the State Council of the People's Republic of China, Wen Jiabao, was on hand to sign the agreement for the 1350MW facility.

Staying on the manufacturing thread, requirements to source equipment locally has shaken the wind market, offering a potential green industry, more jobs and great press to political leaders that implement such measure, but limiting development of a free market offer. In Brazil a 60% local content requirement is in place for projects receiving financing from the BDNES Development Bank, a main source of local financing for wind projects, and project tenders.

Pacific Hydro's Grant says that although it might mean paying a higher price for the equipment, the access to cheaper lines of financing offsets the cost. Plus, since it's applied to all companies that seek financing from the BDNES Development Bank, it has “created level playing field”. He also believes that the requirement has been effective in spurring the local manufacturing market in Brazil.

Key Latin American wind power markets in focus

Brazil

No matter what, one cannot discuss the development of the wind market without mentioning Brazil, Latin America's largest wind power player. Complementing its substantial hydro and biomass resources, wind power has provided an avenue for the country to expand its domestic supply of energy, although the country has not wavered in pushing fossil fuel extraction and energy production either.

Brazil accounted for the lion's share of installed wind capacity growth, adding 1077MW in 2012. The country also has almost 7GW of projects in the pipeline through 2016. Globally, GWEC describes Brazil as “one of the most promising onshore markets for wind energy, at least for the next five years”.

The majority of Brazil's resources, which are estimated by GWEC to be more than 350GW, are mostly in the Northeast with some in the south of the country too. However GWEC says to active sustained development, the country's policy framework must be adapted to offer a support system and greater legal security in the processing of projects.

Current projections envision 16GW of wind power installed in the country by the end of 2021. When looking at 2012, Brazil closed out the year with 2.5GW of installed capacity; enough to power four million households and provide for 2% of national electricity consumption, according to GWEC. Over the year, 40 new wind farms came online, adding about 1GW of new capacity and creating 15,000 new jobs. In terms of investment, the total for 2012 reached US$3.42bn and is expected to reach US$24.5bn by 2020.

Mexico

According to GWEC, Mexico more than doubled its installed wind capacity during 2012, adding 801MW for a total of 1370MW installed. This growth has placed Mexico on the list of 24 countries with more than 1000MW of capacity.

Looking forward, much of Mexico's future will depend on how the process to open its energy sector for private investors evolves. The sector has been under the control of state regulators and a state run oil monopoly Pemex for eight decades. While the announcement is a game changer for the energy sector in general, its focus is to draw investment into its oil and gas sector, which has seen production falter over the last eight years.

Currently, wind projects can be used to supply energy to specific projects, but only the government can feed into the grid. If reforms allow private investors to feed into the transmission lines and the new energy strategy does indeed focus on promoting renewables, then this will become a key market to watch moving forward.

One milestone that occurred in 2012 for Mexico is that new wind capacity was installed outside of the traditional wind rich area of Oaxaca. Although modest (10MW in Baja California and a Grupo Salinas run 28.8MW project in Chipas) it is a sign that wind could reach more parts of this nation.

Argentina

Argentina might represent the country with the greatest untapped potential. The current political and economic scenario does not encourage large-scale investments from private firms. The government's takeover of Repsol and a willingness to intervene in the energy sector, among others, has frozen interest in developing the potential to harness wind.

In 2012, the country added 54MW of new capacity to reach a total of 167MW. Its wind resources are unprecedented, as its southern corridor are essentially one gigantic wind tunnel. GWEC says there are analysts who estimate Argentina alone has the raw wind recourses to supply all of Latin America's wind energy “7 times over again”.

The previously mentioned GEASSA wind farm, slated to be Latin America's largest, is a big deal. But time will reveal if other large-scale projects follow in today's risk scenario.

Chile

As mentioned in the main article, Ernst & Young describes Chile as a rising star. This is fueled in part by government mandates, but also by economics. Apart from large scale hydro projects which have suffered from droughts recently, Chile has very few domestic energy options.

GWEC does not provide a breakdown for Chile, but according the country's National Energy Commission (CNE), Chile's installed wind capacity logged in at 201MW at the end of 2011 and 205MW installed at the end of 2012, with another 97MW in construction and 3250MW in approved projects.

Government mandates, which in 2010 established a renewable energy target of 20% by 2020 (doubling the goal at the time of 10%), were discarded in 2012 as infeasible. However, in January legislators looked to lower technical requirements to get new projects online faster and push the 2020 target to 15-20%, putting renewables back on the table. This year, 2013, is an election year, and energy prices are a recurring issue in the local press. Will the mandate change after a new administration takes office?

The rest

Venezuela, also awash in its own political and economic turmoil, also appears an unlikely candidate for wind investment. In 2012 it did see its first commercial wind farm commissioned for 30MW. The need for energy is dire, with roving blackouts and energy rationing a daily reality. But the aftermath of Chavez is no place for private wind investors, most commentators suggest.

Peru is a new player in the renewables space, although hydro and natural gas resources make it less likely to become a global wind power.

Another country with potential and some signs of interest from the political forces is Colombia. Looking at the possibility of a peace deal with the Farc guerilla group, hitting new records of foreign direct investment and building out basic infrastructure are now greater possibilities, especially as its oil industry pumps out more than a million barrels a day, starting in 2013. State oil firm Ecopetrol received a patent for small-scale wind production technology. But with so many basic needs in the country's regions, will renewables, and wind in particular become a priority?

Uruguay notched its total capacity by 9MW to reach 52MW total. This year has brought even bigger developments as the government says it will develop 1GW of wind power by 2015. The first major development which falls into this plan is at the hands of Paris based Akuo Energy, which will invest US$205mn in two wind farms, totaling 92MW, scheduled for operations at the end of 2013.

Central America saw small but meaningful gains: Nicaragua installed 40MW and Costa Rica increased its tally by 15MW to 147MW installed.

The potential is real, and in some cases wind is now competing to take a spot as an alternative source of power for Latin American economies, but lots of work is yet to be done.

According to GWEC, Brazil now has 11 manufacturers to satisfy local demand. However this supply of equipment is likely to outpace the demand in the mid-term and a logical train of thought is that it will mean an opportunity for manufacturers to supply equipment to projects in other Latin American markets.

Local projects funded by BDNES might not have much choice, but MAKE's Gaylord points out that the higher cost of producing in Brazil, coupled with the downturn in Europe and US, thus shifting vendors eyes to Latin America, make it a hard prospect. Brazil is alone in its enactment of local content production requirements. Argentina has taken similar measures with other sectors. But the economics of building wind equipment make this difficult. Furthermore, the relatively small scale of the rest of the region does not lend well to a profitable manufacturing business, which needs scale.